Introduction: The Power of Control

Imagine a company that doesn’t manufacture goods, sell products, or directly provide services, yet it controls dozens of businesses that do. Through ownership stakes, it directs strategies, manages risks, and reaps rewards. This is the world of the holding company.

From global giants like Berkshire Hathaway to family-owned business groups, holding companies shape economies worldwide. But behind their power lies a challenge: how do you account for the activities of a company whose main asset is ownership of other companies?

That challenge is answered by holding company accounting, a specialised field ensuring that investments, control, and consolidated financial statements are handled with accuracy and transparency.

What is Holding Company Accounting? Definitions & Scope

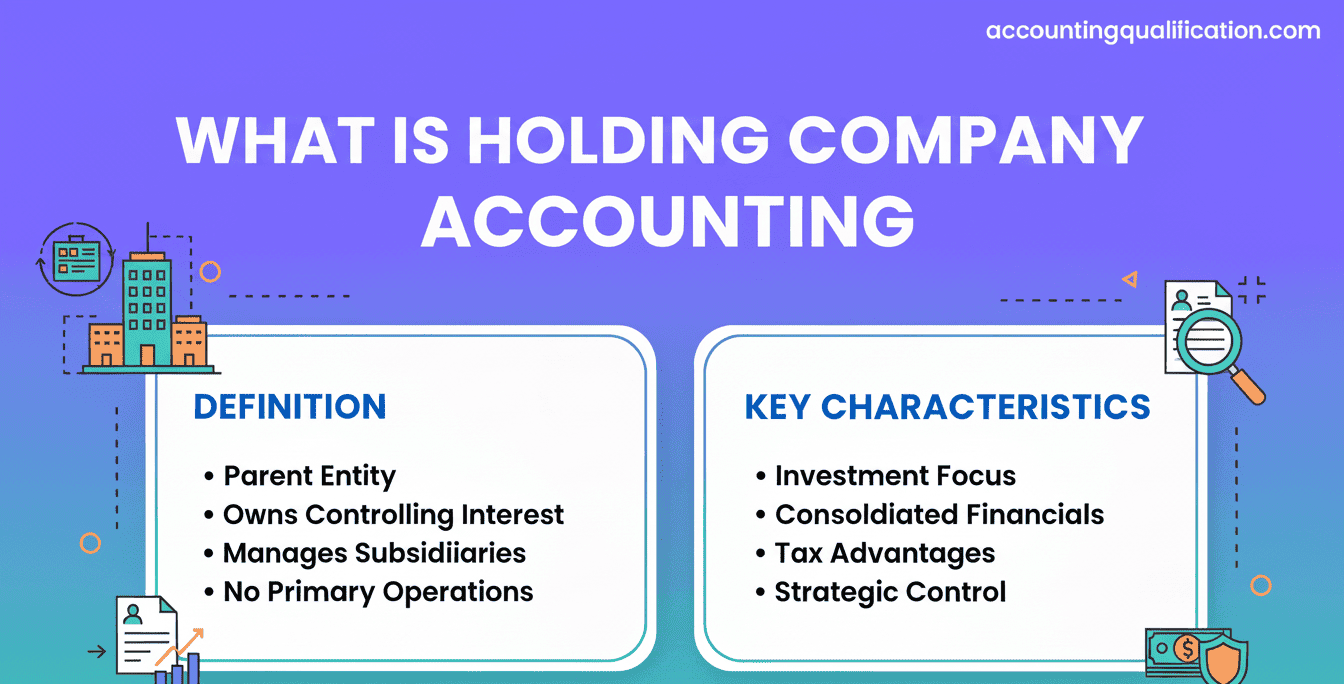

A holding company is a business entity that owns controlling interests in other companies (subsidiaries), but often does not directly produce goods or services itself.

Holding company accounting is the process of recording, managing, and reporting the financial activities of holding companies and their subsidiaries, ensuring compliance, clarity, and transparency.

Key Features

- Control-Oriented: Focuses on ownership, investments, and influence over subsidiaries.

- Consolidated Reporting: Requires combining the financial results of subsidiaries with the parent holding company.

- Compliance-Driven: Must align with global standards such as IFRS 10, IAS 27, or US GAAP ASC 810.

- Complex Structures: Often deals with multinational subsidiaries across industries.

Scope of Holding Company Accounting

- Recording investments in subsidiaries, associates, and joint ventures.

- Preparing consolidated financial statements.

- Eliminating intragroup transactions.

- Recognising minority interests (non-controlling shareholders).

- Handling goodwill and fair value adjustments from acquisitions.

- Managing dividends, loans, and capital transfers within the group.

📌 In short, holding company accounting ensures that investors, regulators, and managers see the true financial picture of the entire group, not just the parent entity.

History & Evolution of Holding Company Accounting

The concept of holding companies is not new, it grew out of industrialisation, expansion, and the desire for businesses to diversify and control multiple enterprises.

Early Developments

- 19th Century: The rise of railroads, utilities, and banks in the United States and Europe led to parent companies controlling smaller entities.

- 1890s (US): New Jersey introduced laws allowing companies to own shares in others, paving the way for holding company structures.

20th Century

- As corporations grew, holding companies became common in sectors like oil, energy, and finance.

- Regulation increased after abuses of monopoly power (e.g., antitrust laws in the US).

- The growth of conglomerates (e.g., ITT, General Electric) made consolidated reporting essential.

Modern Era

- Globalisation expanded holding companies across borders.

- Today, large multinational groups like Alphabet (Google) and Berkshire Hathaway operate as holding companies.

- Standards like IFRS 10 now govern how control and consolidation must be reported.

📌 Holding company accounting evolved alongside corporate expansion, responding to the need for clarity in increasingly complex group structures.

Types of Holding Companies & Objectives

Types of Holding Companies

- Pure Holding Company

- Exists solely to own shares of other companies.

- Example: A family investment company managing stakes in various subsidiaries.

- Mixed Holding Company

- Engages in its own operations while also controlling subsidiaries.

- Example: A tech firm that owns manufacturing subsidiaries but also develops software directly.

- Immediate Holding Company

- A parent that controls another entity but is itself controlled by a higher-level company.

- Intermediate Holding Company

- Sits between the ultimate parent and subsidiaries, often used in multinational structures.

- Investment Holding Company

- Primarily holds investments for generating income (dividends, capital gains).

- Example: Private equity holding companies.

Objectives of Holding Company Accounting

- Unified Financial Reporting – Show the group’s performance as one entity.

- Investor Transparency – Help investors understand the entire structure.

- Compliance – Meet regulatory standards (IFRS, GAAP).

- Eliminate Double Counting – Remove intragroup sales, loans, and dividends.

- Risk Management – Assess overall exposure across subsidiaries.

- Strategic Planning – Provide accurate data for mergers, acquisitions, or divestments.

📌 Holding company accounting is about more than numbers, it ensures trust, efficiency, and strategic clarity in complex business groups.

The Holding Company Accounting Process / Cycle

The process for holding company accounting overlaps with consolidation accounting but focuses specifically on ownership and control relationships.

Step-by-Step Cycle

- Identify Subsidiaries, Associates, and Joint Ventures

- Subsidiary: Parent controls >50% or voting rights.

- Associate: Parent has significant influence (20–50%).

- Joint Venture: Shared control between parties.

- Align Accounting Policies & Periods

- Ensure all subsidiaries use consistent accounting rules and reporting dates.

- Record Investments

- Investments in subsidiaries shown at cost (standalone) or consolidated (group accounts).

- Associates recorded using the equity method.

- Combine Financial Statements

- Add assets, liabilities, revenues, and expenses of the parent and subsidiaries.

- Eliminate Intragroup Transactions

- Cancel sales, loans, dividends, and profits between group companies.

- Recognise Non-Controlling Interest (NCI)

- Show minority shareholders’ share of net assets and income.

- Account for Goodwill and Fair Value Adjustments

- Record premiums paid in acquisitions, test goodwill for impairment.

- Prepare Consolidated Statements

- Income statement, balance sheet, cash flow, and equity changes.

- Disclosures

- Provide detailed notes about subsidiaries, NCI, acquisitions, and accounting policies.

Key Techniques & Tools in Holding Company Accounting

Holding company accounting requires precision, especially when managing multiple subsidiaries across industries and borders.

Techniques

- Elimination Entries

- Removing intragroup sales, expenses, loans, and dividends.

- Prevents overstated income or assets.

- Goodwill Recognition

- Arises when the purchase price of a subsidiary exceeds the fair value of its net assets.

- Requires annual impairment testing.

- Minority Interest Adjustments (Non-Controlling Interest, NCI)

- Reflects the portion of subsidiaries not owned by the parent company.

- Equity Method

- For associates (20–50% ownership), the parent records its share of profit/loss without full consolidation.

- Fair Value Adjustments

- Subsidiary assets/liabilities revalued at acquisition to reflect fair market value.

- Foreign Currency Translation

- Converts subsidiaries’ financials into the parent’s reporting currency.

- Governed by IAS 21.

Tools

- ERP Systems: SAP, Oracle NetSuite, Microsoft Dynamics.

- Consolidation Software: Hyperion Financial Management (HFM), OneStream, Tagetik.

- Cloud Solutions: Workday, Anaplan for multinational reporting.

- Analytics Platforms: Tableau, Power BI for visualising consolidated results.

📌 Tools help holding companies handle complex eliminations, goodwill, and multi-currency adjustments with efficiency.hoose a block

Conclusion

Holding companies are powerful structures that allow businesses to control multiple subsidiaries and diversify across industries and geographies. But with that power comes complexity.

Holding company accounting ensures clarity and transparency by consolidating accounts, eliminating intragroup distortions, and complying with global standards. From Berkshire Hathaway to Alphabet, the strength of holding companies depends on robust accounting practices.

The future will demand even more, automation, ESG integration, and stronger ethics. Holding company accountants will continue to play a vital role as guardians of trust and advisors for growth.

FAQs on Holding Company Accounting

1. What is holding company accounting?

It is the process of recording, managing, and consolidating the financial activities of a holding company and its subsidiaries.

2. What is a holding company?

A company that owns controlling interests in other companies but may not directly engage in operations itself.

3. Why do businesses use holding companies?

To control subsidiaries, diversify risk, protect assets, and optimise tax or legal structures.

4. How are holding companies different from operating companies?

Holding companies own other businesses, while operating companies run day-to-day business activities.

5. What are consolidated financial statements?

Statements that combine the parent and all subsidiaries into one unified report.

6. What are intragroup eliminations?

Adjustments that remove transactions between group companies to prevent double counting.

7. What is goodwill in holding company accounting?

The premium paid when acquiring subsidiaries, above the fair value of net assets.

8. What is non-controlling interest (NCI)?

The portion of a subsidiary’s net assets and profit not owned by the parent company.

9. What accounting standards apply to holding companies?

IFRS 10, IAS 27, and US GAAP ASC 810.

10. What is the equity method?

Used when the parent has significant influence (20–50% ownership) but not control.