What is Cost Accounting

Imagine running a company that makes thousands of products every month. You know what you sell them for, but do you really know what each one costs to make? Without that knowledge, how can you decide what price to charge, which product to promote, or where to cut expenses?

This is where cost accounting comes in. It’s not just about crunching numbers or keeping records; it’s about uncovering the story behind every pound, dollar, and euro a business spends. From the assembly lines of Siemens to the fashion houses of London, cost accounting quietly shapes decisions that drive growth and profit.

In this guide, we’ll explore cost accounting from every angle — what it means, how it evolved, the methods used today, and how it’s changing with technology and globalisation.

Definition and Scope of Cost Accounting

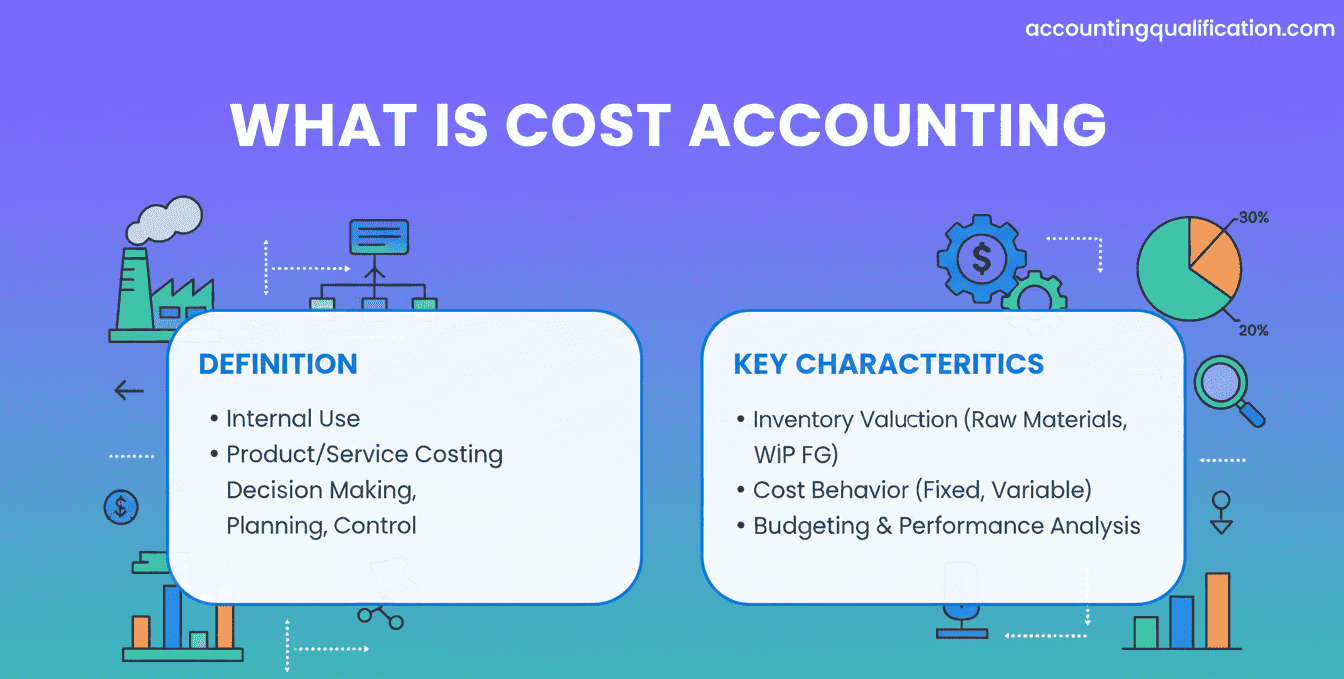

Cost accounting is the process of recording, classifying, analysing, and allocating costs associated with a product, service, or project. Its purpose is to help management control spending, set accurate prices, and improve profitability.

Scope of Cost Accounting

The scope goes beyond manufacturing. It applies to:

- Service organisations (like banks, hospitals, and logistics companies)

- Non-profit institutions (such as charities monitoring resource use)

- Government departments (for budgeting and performance analysis)

- Agriculture and construction (for project and input costing)

In short, cost accounting provides the foundation for effective financial management across all sectors.

History and Evolution

The origins of cost accounting can be traced back to the Industrial Revolution in the 18th century. As factories expanded, business owners needed a way to measure how efficiently they used resources.

Early Development

- 18th and 19th centuries: Textile and steel industries in Britain and America started tracking labour and material costs.

- 1900s: Standard costing and variance analysis emerged as businesses sought to improve efficiency.

- Mid-20th century: Management accounting grew from cost accounting, focusing more on decision-making and strategy.

- Modern era: Technology transformed cost accounting into a data-driven practice integrated with ERP (Enterprise Resource Planning) systems.

Today, cost accounting is not just about measuring costs; it’s about helping organisations make informed, forward-looking decisions.

Types of Cost Accounting

Different businesses use different cost accounting methods depending on their operations. Here are the main types:

1. Standard Costing

In this system, costs are pre-determined and compared with actual costs to identify variances.

Example: A car manufacturer sets a standard cost for steel and labour per unit, then analyses differences to find inefficiencies.

2. Marginal Costing

Focuses on the variable cost of producing one extra unit. It helps businesses with short-term decision-making, such as pricing or production planning.

3. Activity-Based Costing (ABC)

ABC assigns costs to activities rather than departments.

Example: In a logistics company, packaging, transport, and storage costs are tracked separately to identify cost drivers.

4. Job Costing

Used for customised products or services. Each job or project is treated as a separate cost unit.

Example: A construction company calculates costs for each building project individually.

5. Process Costing

Used in continuous production industries such as chemicals or oil refining. Costs are averaged over a large number of identical units.

6. Throughput Accounting

Focuses on maximising output relative to constraints in the production process. It’s common in lean manufacturing systems.

Objectives and Importance of Cost Accounting

The main goal of cost accounting is to provide detailed cost information to management for effective decision-making. Key objectives include:

- Cost Control: Identifying unnecessary expenditure and improving efficiency.

- Cost Reduction: Finding permanent ways to reduce costs without affecting quality.

- Pricing Decisions: Helping businesses set prices that cover costs and yield profits.

- Profitability Analysis: Determining which products, departments, or services are most profitable.

- Inventory Valuation: Providing accurate cost data for financial statements.

- Budgeting and Forecasting: Supporting future financial planning.

In essence, cost accounting turns data into insight, and insight into strategy.

The Cost Accounting Process

Cost accounting follows a logical cycle of data collection, analysis, and reporting.

Step 1: Recording Costs

All direct and indirect costs related to materials, labour, and overheads are recorded.

Step 2: Classifying Costs

Costs are grouped by nature (materials, labour, expenses) or behaviour (fixed, variable, semi-variable).

Step 3: Allocating Costs

Costs that can be directly linked to a product are allocated accordingly.

Step 4: Apportioning Overheads

Indirect costs (like rent or electricity) are distributed among departments based on usage.

Step 5: Analysing and Interpreting

Managers examine cost patterns, compare them to standards, and identify variances.

Step 6: Reporting

Finally, cost reports are prepared to support managerial decisions and strategic planning.

Key Techniques and Tools

Cost accounting uses both traditional and modern tools:

Traditional Techniques

- Standard costing

- Marginal costing

- Absorption costing

- Budgetary control

Modern Techniques

- Activity-Based Costing (ABC)

- Target costing

- Lifecycle costing

- Kaizen costing

- ERP and automation tools

Example tools:

- SAP and Oracle for cost management

- Microsoft Excel and Power BI for analysis

- QuickBooks and Xero for SMEs

What is cost accounting in simple terms?

It’s the process of calculating and analysing the cost of producing goods or services.

How is cost accounting different from financial accounting?

Financial accounting records overall company performance, while cost accounting focuses on internal cost control.

What are the main types of costs?

Fixed, variable, semi-variable, direct, and indirect costs.

What is the purpose of cost accounting?

To help businesses control spending, set prices, and increase profit.

Who uses cost accounting?

Managers, accountants, investors, and decision-makers in both public and private sectors.

What is an example of cost accounting?

A factory tracking labour and material costs to determine the total cost of producing one product.

What is a cost centre?

A department or section where costs are collected, such as maintenance or production.

What is Activity-Based Costing (ABC)?

A method that assigns costs to specific activities to identify inefficiencies.

Why is cost accounting important for small businesses?

It helps them price products accurately and manage limited resources effectively.

How often should cost reports be prepared?

Monthly or quarterly, depending on the business’s size and activity.