Introduction: When Businesses Become Groups

Imagine a fast-growing company that starts buying smaller firms to expand its reach. Soon it owns subsidiaries across different countries, each with its own books, currencies, and reporting rules. Investors, regulators, and shareholders all ask the same question: “How do we see the whole picture?”

This is where consolidation accounting steps in. It’s the art and science of combining multiple sets of accounts into one unified financial statement that reflects the entire group as if it were a single entity.

From mergers and acquisitions to global expansions, consolidation accounting helps businesses present a clear, transparent view of their financial health. Without it, investors would be left piecing together fragmented numbers from dozens of subsidiaries.

But what exactly is consolidation accounting, and why does it matter so much in today’s interconnected economy?

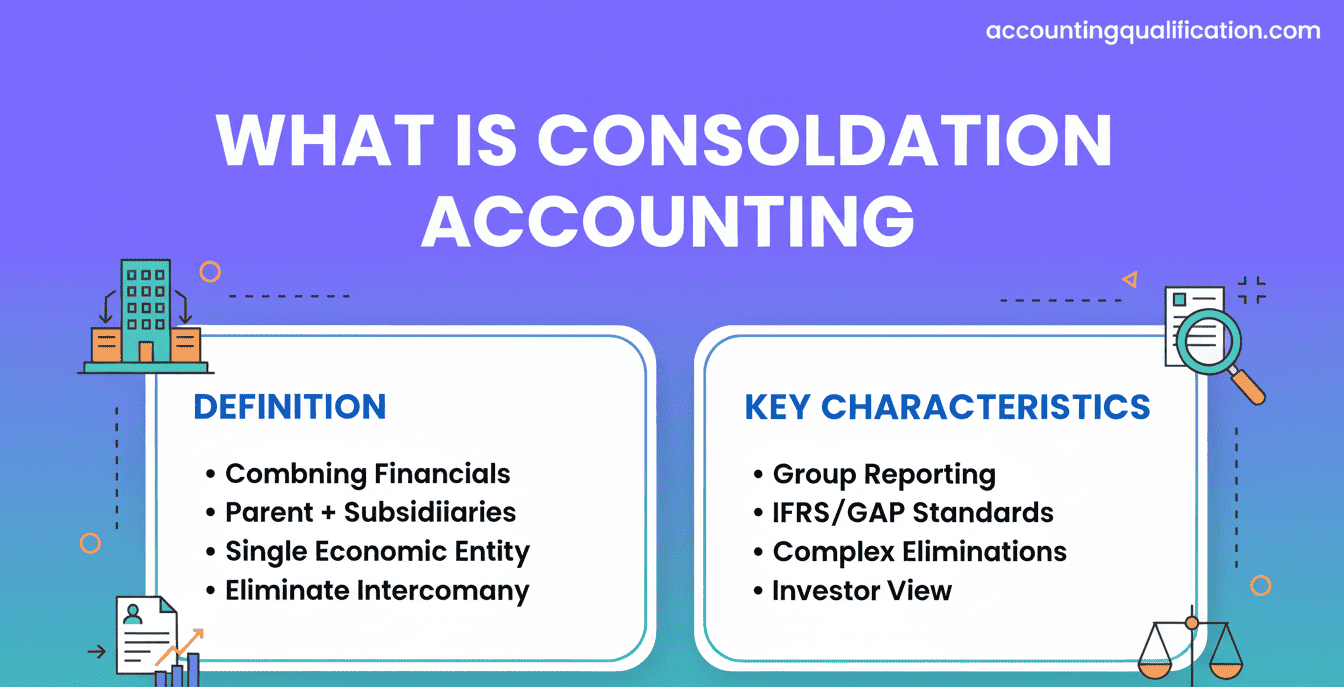

What is Consolidation Accounting? Definitions & Scope

Consolidation accounting is the process of combining the financial statements of a parent company and its subsidiaries into one set of financial statements. The goal is to present the group’s financial position and performance as though it were a single entity.

Key Elements

- Parent Company: The company that controls other businesses (subsidiaries).

- Subsidiaries: Companies controlled by the parent, usually through majority shareholding.

- Group Accounts: The consolidated financial statements representing the parent and all subsidiaries together.

Scope of Consolidation Accounting

- Combining balance sheets, income statements, and cash flows.

- Eliminating intragroup transactions (sales, loans, dividends within the group).

- Adjusting for minority interests (non-controlling shareholders in subsidiaries).

- Ensuring compliance with global standards like IFRS 10 and IAS 27.

- Providing investors with a complete, transparent picture of the group.

👉 In short, consolidation accounting is what makes group reporting possible, ensuring that complex corporate structures don’t confuse stakeholders.

History & Evolution of Consolidation Accounting

Consolidation accounting developed as businesses began to grow beyond single entities, especially during industrialisation and the rise of multinational corporations.

Early Developments

- 19th Century: As railways, banks, and industrial companies grew, holding companies started acquiring subsidiaries. The need for group accounts became clear.

- 1900s: Some US and UK companies experimented with combined statements, though methods varied.

Mid-20th Century

- After World War II, corporations expanded globally. Regulators required clearer group financial statements to protect investors.

- Standard-setting bodies began formalising consolidation principles.

Modern Standards

- International Standards: IFRS 10 (“Consolidated Financial Statements”) defines when and how companies must consolidate.

- US Standards: US GAAP (ASC 810) provides guidance for consolidation.

- Globalisation: Consolidation is now essential for cross-border corporations, mergers, and acquisitions.

📌 Today, consolidation accounting is a cornerstone of transparency in financial markets.

Types / Approaches to Consolidation

There are several ways businesses consolidate accounts, depending on control and ownership structure.

1. Full Consolidation

- Used when the parent has control (usually >50% of voting rights).

- The subsidiary’s assets, liabilities, income, and expenses are fully combined.

- Non-controlling interests (minority shareholders) are shown separately.

2. Proportionate Consolidation

- Rare under IFRS today but sometimes used in joint ventures.

- The parent includes its share of the subsidiary’s assets, liabilities, income, and expenses.

3. Equity Method

- Used when the parent has significant influence but not control (20–50% ownership).

- Investment recorded as a single line item in the balance sheet, adjusted for the parent’s share of profits/losses.

4. Line-by-Line Method (Historical)

- Each line of the subsidiary’s accounts added to the parent’s.

- Still part of full consolidation, but modern standards provide stricter elimination rules.

Objectives & Importance of Consolidation Accounting

Why is consolidation accounting necessary?

Objectives

- Unified Financial Picture – Presenting the group as a single entity.

- Transparency – Preventing “double counting” from intragroup transactions.

- Investor Confidence – Showing true performance of the entire group.

- Regulatory Compliance – Meeting IFRS/GAAP requirements.

- Risk Assessment – Helping stakeholders understand exposure at the group level.

Importance in Today’s Economy

- For Investors: Consolidated reports are easier to analyse than dozens of individual subsidiary accounts.

- For Regulators: Protects markets from misleading reporting.

- For Management: Provides a strategic overview of group performance.

👉 Without consolidation, large corporate groups would look fragmented and confusing.

The Consolidation Accounting Process / Cycle

Consolidation follows a structured process each reporting period.

Step-by-Step

- Identify the Group Structure

- Determine which entities are subsidiaries, associates, or joint ventures.

- Align Accounting Policies

- Ensure all entities use consistent accounting policies.

- Combine Financial Statements

- Add together the assets, liabilities, income, and expenses of parent and subsidiaries.

- Eliminate Intragroup Balances & Transactions

- Cancel out sales, loans, dividends, and profits made between group companies.

- Adjust for Non-Controlling Interests (NCI)

- Show minority shareholders’ share of net assets and profit separately.

- Apply the Equity Method for Associates

- Record the parent’s share of associates’ profits/losses.

- Prepare Consolidated Statements

- Balance sheet, income statement, cash flow, and statement of changes in equity.

- Disclosures

- Provide detailed notes on subsidiaries, NCI, and methods used.

🔑 The key principle: treat the group as one economic entity.

Key Techniques & Tools in Consolidation Accounting

Consolidation accounting is complex, especially for multinational groups. It relies on both traditional principles and modern technologies.

Techniques

- Elimination Entries

- Removing intragroup sales, expenses, loans, and dividends.

- Prevents “double counting” that would inflate revenues or assets.

- Minority Interest Adjustments

- Recognising the share of net income and equity that belongs to non-controlling shareholders.

- Foreign Currency Translation

- When subsidiaries use different currencies, statements are converted into the parent’s reporting currency.

- Governed by IAS 21 (Effects of Changes in Foreign Exchange Rates).

- Fair Value Adjustments

- Assets and liabilities of acquired subsidiaries often need to be restated to fair value.

- Goodwill Recognition

- The premium paid during acquisitions (purchase price – fair value of net assets) is recorded as goodwill.

- Equity Method

- For associates, the parent records its share of net income without full consolidation.

Tools

- ERP Systems: SAP, Oracle NetSuite, Microsoft Dynamics.

- Specialised Consolidation Software: Hyperion Financial Management (HFM), OneStream, Tagetik.

- Cloud Platforms: Workday, Anaplan.

- Data Analytics Tools: Tableau, Power BI for consolidation reporting.

👉 Large corporations often need dedicated consolidation modules within ERP systems to handle complex eliminations, adjustments, and reporting requirements.

Conclusion

Consolidation accounting is the glue that holds complex corporate structures together. It allows investors, regulators, and managers to see the true financial health of a group, without distortions from intragroup transactions or fragmented reports.

From the early days of holding companies to today’s multinational giants, consolidation has evolved into a highly regulated, tech-driven discipline. It is not only about compliance but also about clarity, trust, and strategy.

As technology, ESG requirements, and globalisation reshape the landscape, consolidation accountants will continue to be essential, balancing financial accuracy with transparency and ethics.

FAQs on Consolidation Accounting

1. What is consolidation accounting?

It is the process of combining the financial statements of a parent company and its subsidiaries into one unified set of statements.

2. Why is consolidation accounting important?

It provides a complete picture of the group’s financial performance and avoids misleading duplication of revenues or assets.

3. When is consolidation required?

When a company controls one or more subsidiaries, usually through majority ownership or voting rights.

4. What is a consolidated financial statement?

A single report showing the assets, liabilities, income, and cash flows of the entire group as if it were one company.

5. What are intragroup eliminations?

Adjustments that remove transactions between group companies, such as intercompany sales, loans, or dividends.

6. What is non-controlling interest (NCI)?

The share of a subsidiary’s equity and profit that belongs to minority shareholders, not the parent.

7. What is goodwill in consolidation?

The premium paid when acquiring a subsidiary, above the fair value of its net assets.

8. What are the main methods of consolidation?

Full consolidation, proportionate consolidation (rare today), and the equity method.

9. What is the equity method?

When a parent has significant influence (20–50% ownership), it records its share of the associate’s profit or loss as one line in the accounts.

10. Do all subsidiaries need to be consolidated?

Yes, unless they are immaterial or held for sale (special exemptions apply).