Introduction

When Carillion collapsed in 2018, leaving debts of over £7 billion and tens of thousands of jobs at risk, one question dominated headlines: where were the auditors? The company had received clean audit opinions in the years leading up to its collapse, despite deep financial troubles. This scandal shook trust in auditing, leading to government inquiries and proposals for reform.

Auditing sits at the very heart of the financial system. Every year, billions of pounds flow through companies, charities, and government bodies. Auditors act as independent watchdogs, ensuring that financial statements are true, fair, and reliable. Their role underpins confidence in markets, protects investors, and reassures the public that money is being managed responsibly.

But auditing isn’t just about spotting fraud or errors. It’s also about strengthening corporate governance, transparency, and accountability. In a world shaped by financial scandals, digital disruption, and rising demands for sustainability, auditing has never been more relevant — or more scrutinised.

This first part of our guide explores the foundations of auditing: what it is, where it came from, its main types, objectives, principles, and the processes that define the profession.

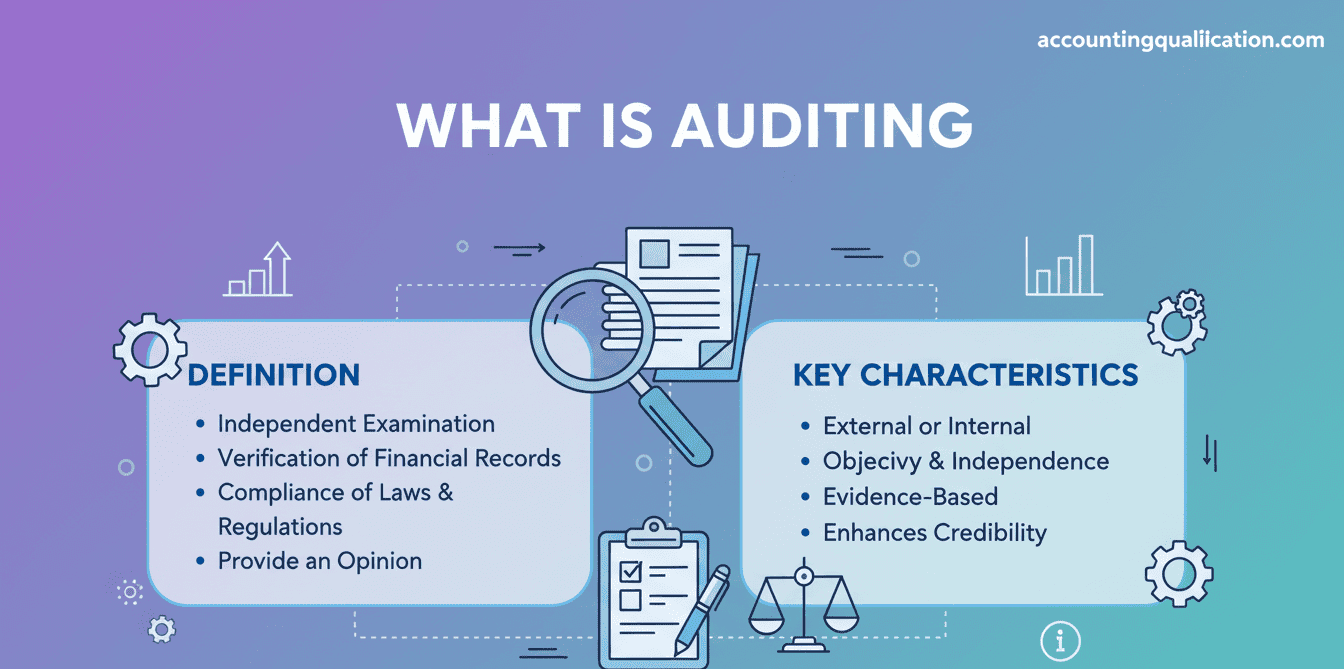

What is Auditing?

Auditing is the systematic examination of financial records, processes, and controls to ensure accuracy, compliance, and reliability.

In the, external financial audits are governed by the Companies Act 2006, with standards set by the Financial Reporting Council (FRC) and aligned with International Standards on Auditing (ISA).

Key Features of Auditing

- Independence – auditors must remain unbiased.

- Evidence-Based – conclusions drawn from verifiable records.

- Compliance-Oriented – checks against laws, standards, and policies.

- Assurance-Focused – provides confidence to stakeholders.

Auditing vs Accounting

- Accounting: Prepares financial information.

- Auditing: Examines and verifies that information.

📌 Example: An accountant records company revenue; an auditor ensures that revenue is real, recorded correctly, and not overstated.

A Detailed History of Auditing

Ancient Origins

- Mesopotamia & Egypt: Early record-keepers reviewed grain, tax, and treasury accounts to prevent corruption.

- Ancient Rome: “Quaestors” examined public accounts and military finances.

Medieval England

- The Exchequer used “tally sticks” to record payments.

- Royal auditors travelled the country to review sheriffs’ tax accounts.

19th Century Industrial Revolution

- The growth of joint-stock companies in the led to rising demand for independent audits.

- Companies Act 1844 required shareholder access to financial records.

- Companies Act 1900 made audits compulsory for many companies.

20th Century

- Expansion of auditing with globalisation and multinational corporations.

- Development of international audit standards.

21st Century

- Enron (2001), WorldCom (2002), Carillion (2018), Wirecard (2020) shook confidence in auditors.

- Led to stronger regulation and reforms, especially in the where the FRC is being replaced by the Audit, Reporting and Governance Authority (ARGA).

Types of Auditing

Auditing takes many forms depending on purpose and scope.

1. External (Statutory) Audit

- Conducted by independent auditors.

- Provides assurance to shareholders that accounts are true and fair.

📌 Example: Deloitte auditing Barclays’ annual financial statements.

2. Internal Audit

- Conducted by employees or in-house teams.

- Focuses on risk management, internal controls, and efficiency.

📌 Example: NHS internal audit reviewing procurement practices.

3. Forensic Audit

- Investigates fraud, corruption, or financial crime.

📌 Example: A forensic audit uncovering procurement fraud in local government contracts.

4. Compliance Audit

- Ensures adherence to laws, regulations, and internal policies.

📌 Example: Checking whether a financial institution complies with anti-money laundering laws.

5. Performance / Value-for-Money Audit

- Evaluates efficiency, economy, and effectiveness.

📌 Example: The NAO auditing government programmes to assess whether taxpayers received value for money.

6. IT Audit

- Reviews systems, cybersecurity, and data integrity.

📌 Example: Auditing HMRC’s digital tax systems for reliability and security.

7. Environmental & ESG Audit

- Focuses on sustainability, carbon reporting, and corporate social responsibility.

📌 Example: Verifying whether a company’s net-zero claims are accurate.

Objectives of Auditing

Auditing serves multiple objectives beyond simple verification.

- Accuracy – ensuring financial statements are correct.

- Compliance – confirming adherence to legal and regulatory frameworks.

- Fraud Detection & Prevention – identifying irregularities and strengthening controls.

- Accountability – holding management responsible for decisions.

- Transparency – providing reliable information to stakeholders.

- Improved Governance – helping boards oversee risk and strategy.

📌 Scenario: If a company reports £1bn in profits, an audit ensures those profits are not inflated by creative accounting or hidden liabilities.

Principles & Standards of Auditing

Auditing is governed by a set of principles designed to ensure quality and integrity.

Core Principles

- Integrity: Auditors must act honestly.

- Objectivity: Free from bias or conflict of interest.

- Confidentiality: Protect client information.

- Professional Competence: Maintain up-to-date skills.

- Independence: Critical to credibility.

International and Standards

- International Standards on Auditing (ISA): Applied globally.

- Adaptations: Overseen by the FRC.

- Companies Act 2006: Legal framework for statutory audits.

- Corporate Governance Code: Requires audit committees in listed companies.

The Audit Process (Step by Step)

Auditing follows a structured cycle.

Step 1: Planning & Risk Assessment

- Understand the business, environment, and risks.

📌 Scenario: Auditing a construction company, auditors assess risks like project delays and cost overruns.

Step 2: Internal Control Evaluation

- Test whether company controls are robust.

📌 Scenario: Reviewing payroll controls to ensure no “ghost employees.”

Step 3: Evidence Collection

- Examine financial records, invoices, bank statements.

- Use sampling and data analytics.

📌 Scenario: Auditors test a sample of revenue transactions for validity.

Step 4: Substantive Testing

- Detailed checking of balances and transactions.

📌 Scenario: Verifying that reported assets actually exist.

Step 5: Analytical Procedures

- Compare ratios, trends, and benchmarks.

📌 Scenario: An unusual spike in expenses triggers deeper investigation.

Step 6: Audit Reporting

- Issue an audit opinion:

- Unqualified (clean)

- Qualified (with issues)

- Adverse (misleading accounts)

- Disclaimer (insufficient evidence)

Step 7: Follow-Up

- Management letters highlight weaknesses and recommendations.

Techniques and Tools in Auditing

Auditors use a mix of traditional techniques and modern technologies to gather evidence and form opinions.

Core Techniques

- Sampling

- Auditors cannot test every transaction, so they sample a representative selection.

📌 Example: Out of 100,000 sales invoices, auditors might check 500 chosen systematically.

- Auditors cannot test every transaction, so they sample a representative selection.

- Confirmations

- Direct verification from third parties.

📌 Example: Confirming customer balances directly with clients.

- Direct verification from third parties.

- Observation

- Watching processes in real time.

📌 Example: Observing an inventory count at a warehouse.

- Watching processes in real time.

- Inspection

- Reviewing documents, contracts, and records.

- Analytical Procedures

- Comparing ratios, trends, and benchmarks.

- Reperformance

- Recalculating figures to confirm accuracy.

Modern Tools

- Data Analytics Software (ACL, IDEA, Power BI).

- ERP Audit Tools (SAP Audit Management).

- AI & Machine Learning – spotting anomalies.

- Blockchain Auditing – verifying crypto and distributed ledger transactions.

- Continuous Auditing Systems – real-time monitoring of transactions.

Real-World Case Studies

1. Enron (2001, US but globally influential)

Auditors at Arthur Andersen failed to challenge complex financial structures. Collapse led to the creation of Sarbanes–Oxley Act and stricter standards worldwide.

2. Carillion (UK, 2018)

Received clean audit opinions before collapse. Parliament accused auditors of “failing in their duty to warn.” Sparked calls for audit reform.

3. Wirecard (Germany, 2020)

EY signed off accounts despite a €1.9bn cash hole. Highlighted global audit challenges in fintech.

4. Patisserie Valerie (UK, 2019)

Forensic audits discovered a £94m accounting fraud. Raised concerns about audit oversight in mid-sized companies.

5. NAO Performance Audits

UK’s National Audit Office conducts audits beyond financial accuracy — checking whether taxpayers get value for money. Example: reviews of HS2 spending and NHS efficiency.

Common Mistakes in Auditing

- Over-reliance on client information without sufficient evidence.

- Weak scepticism – failing to challenge management claims.

- Insufficient sampling – missing material misstatements.

- Inadequate IT knowledge – overlooking cyber risks.

- Poor communication – issuing overly technical reports.

Limitations of Auditing

- Sampling Risk – auditors test samples, not all transactions.

- Collusion – fraud may bypass controls if multiple staff collude.

- Judgement Areas – accounting estimates rely on assumptions.

- Time & Cost Constraints – audits are limited by deadlines and budgets.

- Expectation Gap – the public often expects auditors to detect all fraud, but this is not their mandate.

Ethics in Auditing

Ethics is central to auditing credibility.

- Independence: No financial or personal interest in the client.

- Objectivity: Evidence-based, not influenced by management.

- Integrity: Honest reporting, even if unfavourable.

- Confidentiality: Protecting client data.

- Professional Skepticism: Questioning rather than accepting at face value.

📌 Example: After the Carillion scandal, MPs accused auditors of being “too cosy” with clients, showing why independence matters.

Careers in Auditing

Career Paths

- External Auditor – working in firms (Big Four, mid-tier, or local).

- Internal Auditor – embedded in corporations or public bodies.

- Government Auditor – NAO, HMRC, or local authority audit teams.

- Forensic Auditor – specialising in investigations.

- IT Auditor – focusing on systems and cybersecurity.

A Day in the Life (External Auditor Example)

- Morning: Team planning meeting.

- Midday: Testing revenue recognition transactions.

- Afternoon: Interviewing client finance staff.

- Evening: Preparing working papers and risk assessments.

Skills Needed

- Strong accounting and auditing knowledge.

- Legal and regulatory awareness.

- Analytical and IT skills.

- Communication and report-writing.

- Professional scepticism and ethics.

Salary Ranges

- Graduate/trainee: £26k–32k

- Newly qualified: £40k–50k

- Manager: £60k–80k

- Partner/director: £100k–200k+

Future Trends in Auditing

- AI & Data Analytics

- Continuous risk assessment and fraud detection.

- Blockchain Auditing

- Smart contracts and transparent ledgers.

- Sustainability & ESG Audits

- Verifying climate disclosures and ESG metrics.

- Real-Time/Continuous Auditing

- Moving from annual to ongoing assurance.

- Audit Reform in the

- Creation of ARGA to replace FRC.

- Mandatory joint audits proposed for large firms.

- Cybersecurity Audits

- Increasing focus on digital resilience.

Conclusion

Auditing is more than a technical exercise; it is a cornerstone of trust, governance, and accountability. From tally sticks in medieval England to AI-powered continuous auditing today, the mission remains the same: to give stakeholders confidence in financial information.

Yet the profession faces challenges: scandals, expectation gaps, and technological disruption. The future of auditing lies in being more independent, more digital, and more forward-looking. Done well, auditing strengthens markets, protects investors, and sustains public trust.