Introduction

Imagine a start-up founder pitching to investors. She talks passionately about her product, her market, her team. Then comes the inevitable question: “What do your numbers look like?” The room falls silent.

Whether it’s a neighbourhood café, a growing tech firm, or a multinational conglomerate, numbers tell the story of a business. And those numbers are recorded, analysed, and presented through business accounting.

Accounting is often called the “language of business” — and for good reason. It translates every sale, expense, asset, and liability into insights that guide survival and growth. Without accounting, businesses would be like pilots flying without instruments.

But what exactly is business accounting? How did it evolve, and why is it so crucial in today’s data-driven economy? Let’s begin with the basics.

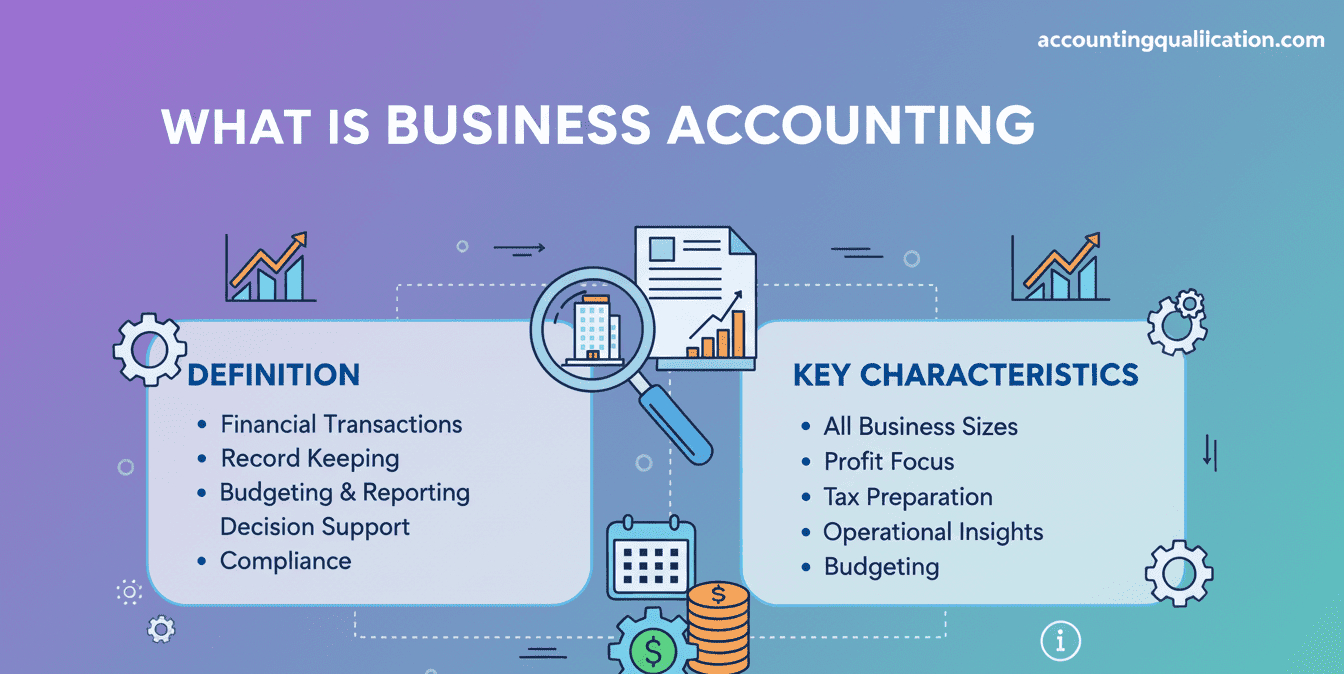

What is Business Accounting? Definitions & Scope

Business accounting is the systematic recording, analysing, and reporting of a business’s financial transactions. It ensures that managers, investors, regulators, and other stakeholders understand the financial health of an organisation.

Key Characteristics

- Universal: Applies to small shops, medium enterprises, and global corporations.

- Decision-Oriented: Provides information for budgeting, investment, and operations.

- Compliance-Driven: Ensures businesses follow tax and regulatory requirements.

- Historical & Forward-Looking: Records past events while enabling forecasts.

Scope of Business Accounting

- Recording daily transactions (sales, purchases, payroll).

- Preparing financial statements (balance sheet, income statement, cash flow).

- Managing taxes and compliance with local laws.

- Cost control and budgeting.

- Internal analysis for decision-making.

- Audit and assurance activities.

- Supporting funding and investment decisions.

👉 In essence, business accounting is the financial heartbeat that keeps organisations alive and credible.

History & Evolution of Business Accounting

Accounting has been around as long as trade itself. The story of business accounting is closely linked to human civilisation’s progress.

Ancient Civilisations

- Mesopotamia (c. 3,000 BCE): Merchants used clay tablets to track trade.

- Egypt & Rome: Accounting supported tax collection and public works.

- India & China: Detailed ledgers and administrative records emerged early.

Middle Ages & Renaissance

- Double-entry bookkeeping (15th century): Formalised by Luca Pacioli, this innovation became the foundation of modern accounting.

Industrial Revolution (18th–19th Century)

- Growth of factories and railways required structured financial reporting.

- Owners and shareholders needed standardised records to track performance.

20th Century

- The rise of limited companies increased the need for accountability.

- Professional bodies such as the AICPA (US), ICAEW (UK), and IFAC (global) established ethical standards.

- Tax laws and government regulations formalised accounting practices worldwide.

21st Century

- Shift from paper ledgers to cloud-based systems.

- AI, automation, and big data transformed how transactions are recorded and analysed.

- Businesses now report not just financial results, but also social and environmental impact.

📌 From ancient tablets to artificial intelligence, business accounting has always adapted to meet the needs of commerce.

Types of Business Accounting

Business accounting isn’t one-size-fits-all. Different branches focus on different aspects of financial management.

1. Financial Accounting

- Prepares reports for external stakeholders (investors, regulators, creditors).

- Example: A company’s annual financial statements filed with regulators.

2. Management Accounting

- Provides internal reports for managers.

- Example: Budgeting and forecasting at a retail chain.

3. Cost Accounting

- Tracks and controls the costs of goods or services.

- Example: A furniture maker calculating the cost of producing each chair.

4. Tax Accounting

- Ensures compliance with local tax laws and planning strategies.

- Example: Preparing corporate tax returns.

5. Auditing

- Internal or external review of accounts to ensure accuracy.

- Example: Independent audit of a manufacturing firm’s accounts.

6. Forensic Accounting

- Investigates fraud or irregularities.

- Example: A forensic accountant reviewing books after suspected embezzlement.

👉 These categories together provide a full view of a business’s financial reality — past, present, and future.

Objectives & Importance of Business Accounting

Every business, regardless of size, needs accounting. Its objectives go beyond record-keeping.

Key Objectives

- Compliance: Meeting legal and tax requirements.

- Performance Tracking: Understanding profits, losses, and financial health.

- Decision-Making: Guiding managers in pricing, investments, and resource allocation.

- Investor Relations: Providing confidence to investors and lenders.

- Fraud Prevention: Ensuring accountability and detecting irregularities.

- Strategic Planning: Supporting long-term growth and sustainability.

Importance in Today’s World

- For SMEs: Helps secure loans and attract investors.

- For Start-ups: Provides credibility in fundraising rounds.

- For Large Firms: Ensures transparency and maintains global reputation.

👉 Business accounting is not just about compliance; it’s about sustainability, growth, and trust.

The Business Accounting Process / Cycle

Like corporate accounting, business accounting follows a structured cycle.

Step-by-Step Cycle

- Recording Transactions

- Capturing sales, purchases, payroll, and expenses.

- Journal Entries

- Recording into the general journal.

- Posting to Ledger

- Classifying into accounts (cash, debtors, creditors).

- Trial Balance Preparation

- Checking that debits equal credits.

- Adjustments

- Accounting for depreciation, accruals, and provisions.

- Financial Statements

- Income statement, balance sheet, and cash flow.

- Audit/Review

- Ensuring accuracy and compliance.

- Reporting & Analysis

- Presenting results to managers, investors, and regulators.

🔄 This cycle repeats periodically — monthly, quarterly, or annually.

Techniques & Tools in Business Accounting

Business accounting blends traditional methods with modern digital innovations. Both are essential for accuracy, efficiency, and insight.

Traditional Techniques

- Double-Entry Bookkeeping

Every transaction has equal debit and credit entries, ensuring balance and accuracy. - Ratio Analysis

Key ratios (profitability, liquidity, solvency, efficiency) assess performance. - Budgeting & Forecasting

Planning income and expenditure, comparing actual vs expected results. - Cash Flow Management

Tracking inflows and outflows to prevent liquidity crises. - Cost Allocation

Distributing overheads fairly across departments, projects, or products.

Modern Tools

- Cloud Accounting Software (Xero, QuickBooks, FreshBooks)

Ideal for SMEs, offering remote access, automation, and integration with banking. - ERP Systems (SAP, Oracle NetSuite, Microsoft Dynamics)

Large firms use these to integrate finance, HR, supply chain, and operations. - Data Analytics Tools (Tableau, Power BI)

Help visualise financial data and generate forecasts. - Artificial Intelligence

Automates reconciliations, detects anomalies, and enhances fraud prevention. - Blockchain

Provides tamper-proof records of transactions, boosting transparency.

👉 The future of accounting is hybrid: timeless principles applied with cutting-edge tools.

Conclusion

Business accounting is the lifeblood of commerce. From local enterprises to multinational giants, it ensures that numbers tell the true story of performance, risk, and opportunity.

The history of accounting proves its resilience and adaptability — from clay tablets to cloud dashboards. Today, it is about more than financial reporting: it is about ethics, sustainability, and strategy.

The future of business accounting lies in technology-driven practices, global standards, and socially responsible reporting. Accountants who master both traditional principles and modern tools will continue to be invaluable to businesses worldwide.

FAQs on Business Accounting

1. What is business accounting?

It’s the process of recording, analysing, and reporting a business’s financial transactions.

2. Why is business accounting important?

It ensures compliance, supports decisions, tracks performance, and builds trust with stakeholders.

3. What’s the difference between business and corporate accounting?

Business accounting applies to organisations of all sizes; corporate accounting is more specialised for large corporations.

4. What are the main types of business accounting?

Financial, management, cost, tax, auditing, and forensic accounting.

5. How often should businesses update their accounts?

Ideally daily, but formal statements are prepared monthly, quarterly, or annually.

6. Do small businesses need accountants?

Yes, even the smallest businesses benefit from accurate bookkeeping and tax compliance.

7. What is the accounting cycle?

The process from recording transactions to preparing financial statements and reports.

8. What software is used for business accounting?

Popular options include QuickBooks, Xero, FreshBooks, SAP, and Oracle.

9. What is double-entry bookkeeping?

A system where every transaction has equal debit and credit entries.

10. Can accounting prevent business failure?

It can’t guarantee survival, but it provides the insight needed to avoid risks and manage cash flow.