Introduction

Taxes. For most of us, the word sparks a familiar mix of obligation and unease. Deadlines from HMRC, forms to complete, numbers to check, and the nagging fear of making an error that could lead to penalties. Yet behind the perceived complexity lies something essential: tax accounting.

In the, taxation funds the very fabric of society. In 2022/23, HM Revenue & Customs collected over £786 billion in taxes, the highest amount on record. That money keeps the NHS running, maintains roads and railways, pays teachers and police officers, and sustains countless public services. None of this would be possible without robust tax accounting systems ensuring money flows from businesses and individuals into government coffers.

But tax accounting is more than just compliance. Done well, it becomes a tool for financial strategy, efficiency, and foresight. Consider a start-up in Manchester, unsure how to manage its R&D credits. Without proper tax advice, it could miss out on tens of thousands of pounds in savings — funds that might otherwise fuel innovation or create new jobs. Or take a self-employed web developer in Bristol: with effective tax planning, they can structure income and expenses to keep more of their hard-earned money while staying compliant.

So, what exactly is tax accounting? How did it evolve, why is it important, and where is it heading in a digital-first, AI-driven world? This comprehensive guide will walk you through everything you need to know, from ancient history to the latest trends in blockchain and green taxation.

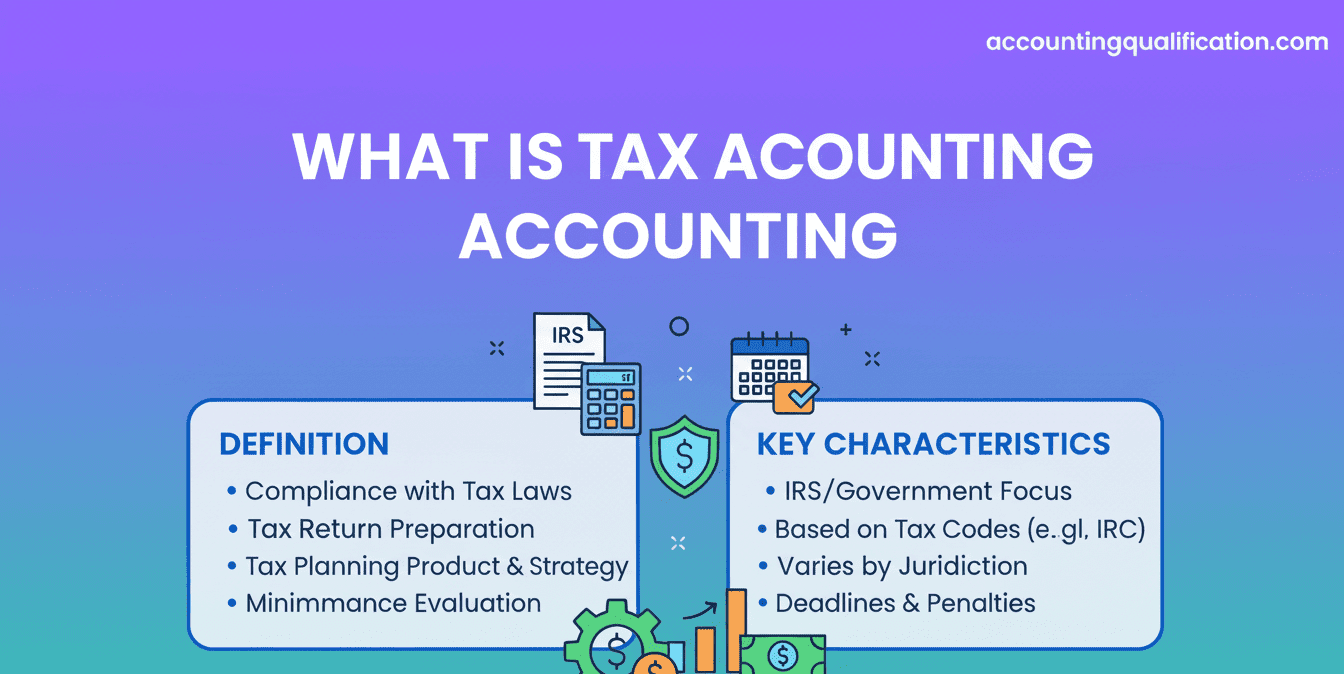

What is Tax Accounting?

At its simplest, tax accounting is the process of calculating, preparing, and reporting taxes owed in line with government regulations. It differs from general accounting because its focus isn’t on showing financial performance to shareholders but on ensuring compliance with tax laws.

In the, tax accounting is shaped by a web of legislation:

- Income Tax Act – for individuals’ income.

- Corporation Tax Act – for companies’ profits.

- Value Added Tax Act – for VAT.

- Inheritance Tax Act – for estates and transfers of wealth.

Benefits of Effective Tax Accounting

Effective tax accounting is far more than just a legal obligation; it’s a powerful driver for financial health and strategic growth. For both businesses and individuals, mastering tax accounting principles or engaging expert help can lead to significant advantages.

Financial Savings & Optimisation

One of the most immediate benefits is the potential for substantial cost savings. Proper tax accounting ensures you utilise every legitimate relief, allowance, and exemption available under law. This might include claiming capital allowances for asset purchases, optimising pension contributions, or leveraging schemes like R&D tax credits for innovation. Minimising your tax liability through smart, legal strategies means more capital remains in your hands, ready for investment, expansion, or personal savings.

Ensured Compliance & Reduced Risk

Navigating the complex landscape of tax law can be daunting. Effective tax accounting provides peace of mind by ensuring full compliance with HMRC regulations. This meticulous approach significantly reduces the risk of errors, penalties, and time-consuming audits. By maintaining accurate records and understanding deadlines, you avoid costly mistakes and potential legal repercussions, safeguarding your financial reputation.

Strategic Decision-Making & Growth

Beyond compliance, robust tax accounting is a vital tool for strategic planning. It offers clear insights into your financial position, allowing for informed decisions about future investments, business restructuring, or personal wealth management. Understanding the tax implications of various scenarios – from hiring new staff to acquiring new assets – empowers you to make choices that align with your long-term financial goals and support sustainable growth.

Enhanced Cash Flow Management

By accurately forecasting tax liabilities and strategically timing payments, effective tax accounting aids in better cash flow management. It prevents unexpected tax bills from disrupting operations or personal finances, allowing for more predictable budgeting and resource allocation. This proactive approach ensures liquidity and stability, crucial for both day-to-day operations and future planning.

The world of tax accounting is undergoing a profound transformation, driven by rapid technological advancements and evolving regulatory demands. The shift towards digitalisation is redefining how taxes are prepared, reported, and managed, ushering in an era of greater efficiency, transparency, and data-driven insights. Understanding these emerging trends is crucial for anyone involved in financial management.

The Digital Evolution of Tax Accounting

The journey from manual ledgers to integrated digital systems is accelerating. Governments worldwide, including the UK with its Making Tax Digital (MTD) initiative, are mandating digital record-keeping and submissions. This push for digitalisation is laying the groundwork for more sophisticated technologies to reshape the industry.

- Making Tax Digital (MTD): Mandatory digital record-keeping and submissions are streamlining compliance for VAT, Income Tax Self Assessment (ITSA), and eventually Corporation Tax. This requires businesses to use HMRC-compatible software.

- Artificial Intelligence (AI) & Machine Learning (ML): AI is automating repetitive tasks like data entry, reconciliation, and expense categorization. It also enhances error detection, identifies anomalies for fraud prevention, and provides predictive analytics for tax forecasting and strategic planning.

- Cloud Accounting Platforms: Solutions like Xero, Sage, and QuickBooks offer real-time data access, collaborative features, and seamless integration with various tax software. This enables remote work, improves data accuracy, and simplifies compliance.

- Blockchain & Distributed Ledger Technology (DLT): While still nascent in tax, blockchain’s potential for enhanced transparency, immutability, and security in transaction records could revolutionise audit processes and cross-border tax reporting, reducing disputes and improving trust.

- Data Analytics: Tax professionals are increasingly using big data analytics to gain deeper insights into financial data, identify tax efficiencies, assess risks, and model the impact of different tax strategies.

- Cybersecurity: With increased digital data, robust cybersecurity measures become paramount to protect sensitive financial information from breaches and ensure data integrity.

These innovations promise not only to simplify compliance but also to empower businesses and individuals with unprecedented control and insight into their tax affairs, moving tax accounting from a reactive process to a proactive strategic function.

Choosing the Right Tax Accounting Professional

While many individuals and businesses manage basic tax affairs themselves, the complexities of tax law often necessitate professional guidance. Choosing the right tax accounting professional is a critical decision that can lead to significant savings, ensure compliance, and provide invaluable peace of mind. But how do you find the best fit for your specific needs?

When to Consider Hiring a Tax Professional

You might benefit from professional help if you:

- Have complex income streams: Multiple jobs, rental properties, freelance income, or investments.

- Run a business: Especially if it’s growing, has employees, or deals with VAT and corporation tax.

- Are dealing with significant life changes: Marriage, divorce, inheritance, starting a family, or selling major assets.

- Have international income or assets: Navigating cross-border tax rules requires specialised knowledge.

- Want to optimise your tax position: To ensure you’re legally taking advantage of all available reliefs and allowances.

- Simply lack the time or confidence: Tax can be daunting, and professionals save you both time and stress.

What to Look for in a Tax Accountant or Adviser

Not all professionals are created equal. Consider these factors when making your choice:

- Qualifications and Accreditation: Look for individuals or firms regulated by professional bodies such as the ICAEW (Institute of Chartered Accountants in England and Wales), ACCA (Association of Chartered Certified Accountants), or the ATT (Association of Taxation Technicians). These accreditations signify expertise and adherence to ethical standards.

- Experience and Specialisation: Does the professional have experience with your specific industry, business type (e.g., sole trader, limited company), or personal circumstances (e.g., expatriate tax, inheritance tax planning)? A specialist will have deeper knowledge relevant to your situation.

- Client Testimonials and Reputation: Check online reviews, ask for references, or seek recommendations from trusted contacts. A strong reputation often indicates reliable and effective service.

- Fee Structure: Understand how they charge – hourly, fixed fee, or percentage-based. Ensure transparency and that their fees align with your budget and the scope of work required.

- Communication Style: Good communication is key. Choose someone who explains complex tax concepts clearly, is responsive to your queries, and keeps you informed.

- Use of Technology: In the age of Making Tax Digital (MTD), ensure they are proficient with MTD-compliant software and comfortable using cloud-based platforms if that’s your preference.

- Insurance: Verify that they hold professional indemnity insurance, offering protection in case of errors or negligence.

By carefully evaluating these aspects, you can find a tax accounting professional who not only manages your compliance needs but also becomes a valuable partner in your financial success.

Key Features of Tax Accounting

- Rule-driven: Follows HMRC regulations, not IFRS or GAAP.

- Calculation-based: Determines taxable income, which may differ from accounting profit.

- Adjustments-focused: Adds back non-deductible expenses (like client entertainment) and applies reliefs (like capital allowances).

- Outcome-specific: The end goal is compliance and optimisation of tax liability.

Tax Accounting vs Financial Accounting

Imagine a company makes £500,000 in accounting profit. Financial accounts will present this as “profit before tax.” Tax accounting adjusts this figure — adding back expenses not allowed for tax, applying allowances, and calculating the corporation tax payable (25% as of 2023). The result? The “taxable profit” could be significantly higher or lower than the accounting profit.

A Brief History of Tax Accounting

Ancient and Medieval Roots

Taxation is not a modern invention. Ancient Egypt had scribes who meticulously recorded harvests, ensuring the Pharaoh’s share was collected. In Ancient Rome, citizens paid tributum to fund armies and public works.

In England, one of the earliest records of systematic taxation was the Domesday Book (1086) commissioned by William the Conqueror. It catalogued land, property, and resources across the kingdom — essentially an early tax register.

18th and 19th Century Developments

The first formal income tax in the was introduced in 1799 by William Pitt the Younger to fund war against Napoleon. Though initially temporary, it became permanent in 1842 under Sir Robert Peel. This required new systems of accounting to track income and deductions.

As the Industrial Revolution expanded commerce, governments introduced taxes on profits, imports, and wages. Accountants developed more sophisticated methods to ensure compliance and fairness.

20th Century to Present

- 1909: “People’s Budget” introduced new taxes on land and wealth.

- 1944: Pay As You Earn (PAYE) was launched, automating income tax collection for employees.

- 1973: The introduced Value Added Tax (VAT), now one of the largest revenue sources.

- 2009: HMRC replaced paper self-assessment filing with mandatory online submissions.

- 2019 onwards: Making Tax Digital (MTD) began, signalling a shift to fully digital tax accounting.

Tax accounting today blends centuries-old principles of fairness with cutting-edge technologies like AI and blockchain.

Types of Tax Accounting

Tax accounting is not a monolith. Different taxpayers face different rules.

1. Personal Tax Accounting

Covers income tax, capital gains tax, and inheritance tax.

Example: A self-employed consultant must record business expenses, calculate net profit, and file an annual self-assessment.

2. Corporate Tax Accounting

Covers corporation tax, VAT, and payroll taxes.

Example: A medium-sized retailer must handle quarterly VAT returns, PAYE for staff, and corporation tax at year-end.

3. International Tax Accounting

Involves cross-border transactions, double taxation treaties, and transfer pricing.

Example: A-based multinational with operations in Germany must ensure profits are allocated fairly between jurisdictions.

4. Indirect Tax Accounting

Focuses on VAT, excise duties, and customs.

Example: An e-commerce store must apply the correct VAT rate for and EU customers, adjusting after Brexit rule changes.

5. Estate and Trust Tax Accounting

Manages inheritance tax and trust distributions.

Example: A family trust transferring property to beneficiaries must calculate inheritance tax liabilities and exemptions.

By breaking tax accounting into these categories, we see its relevance across every aspect of financial life.

Objectives of Tax Accounting

The main objectives include:

- Accurate Calculation – ensuring the correct amount of tax is paid.

- Compliance – avoiding fines and audits.

- Optimisation – legally minimising tax through reliefs and allowances.

- Planning – aligning tax with long-term financial goals.

- Transparency – enabling stakeholders to see obligations clearly.

The Tax Accounting Cycle: Step by Step

- Record Transactions – incomes, expenses, and assets.

- Classify – identify what’s taxable and what’s not.

- Adjust – apply deductions, disallowances, and allowances.

- Calculate Liability – determine tax payable.

- File Returns – submit via HMRC systems.

- Pay Tax – ensure timely payment.

- Maintain Audit Readiness – keep records for at least six years.

Techniques and Tools in Tax Accounting

Techniques

- Capital Allowances – Deduct asset depreciation for tax purposes.

- Transfer Pricing – Align cross-border transactions with OECD rules.

- Deferred Tax – Recognise future tax effects of current differences.

- Tax Planning – Timing of expenses and income to minimise liabilities.

Tools

- HMRC MTD-compliant software – mandatory for VAT-registered businesses.

- Cloud Platforms (Xero, Sage, QuickBooks).

- AI and Data Analytics – automating error detection and forecasting.

- Blockchain – future potential for secure, transparent tax reporting.

Real-World Case Studies

1. Small Business Relief

A Manchester café invests £50,000 in kitchen equipment. By using Annual Investment Allowance, it deducts the full cost, saving over £12,500 in corporation tax.

2. Multinational Transfer Pricing

A-based tech giant must allocate profits between, Ireland, and US operations. Failure to comply could trigger double taxation, so tax accounting ensures fair allocation.

3. Freelancer Tax Efficiency

A freelance designer claims allowable expenses (home office, software, travel), reducing taxable income by £8,000 and saving £3,200 in income tax.

4. Inheritance Planning

A wealthy individual structures assets into a trust. With proper tax accounting, inheritance tax is reduced from 40% of estate value to a significantly lower figure.

Common Mistakes in Tax Accounting

- Missing HMRC deadlines.

- Failing to claim allowances (e.g., R&D credits).

- Incorrect VAT application after Brexit.

- Poor record-keeping.

- Misreporting foreign income.

Limitations of Tax Accounting

- Complexity – tax code exceeds 17,000 pages.

- Cost – professional fees can be high.

- Constant Change – annual Budget updates.

- Ethical Dilemmas – balancing avoidance vs social responsibility.

Ethics: Avoidance vs Evasion

- Tax Avoidance: Legal but often criticised (e.g., Starbucks shifting profits offshore).

- Tax Evasion: Illegal and punishable (concealing income, falsifying records).

Public pressure increasingly demands companies not only follow the law but act responsibly.

Careers in Tax Accounting

Tax accounting offers varied career paths:

- Personal Tax Adviser

- Corporate Tax Specialist

- International Tax Consultant

- HMRC Inspector

Salaries

- Graduate trainee: £28k–35k

- Qualified accountant: £45k–70k

- Senior tax manager: £100k+

A day in the life of a tax accountant may involve analysing legislation changes in the morning, meeting with clients midday, and filing compliance reports in the afternoon.

Future Trends

- Making Tax Digital – full digitalisation by 2026.

- AI and Automation – automating compliance and forecasting.

- Blockchain – tamper-proof transaction tracking.

- Green Taxes – carbon levies, incentives for renewables.

- Global Minimum Tax – OECD reforms to ensure fairness across borders.

- Crypto Taxation – HMRC now requires crypto reporting.

Conclusion

Tax accounting is not just about balancing books or avoiding penalties. It’s a cornerstone of financial health and societal stability. From the Domesday Book to AI-driven compliance, the discipline has constantly evolved to meet new challenges.

For businesses, effective tax accounting unlocks growth. For individuals, it secures financial peace of mind. For society, it funds public services and infrastructure. The future promises more digitalisation, more global alignment, and more scrutiny — but also more opportunities for those who master the art of tax accounting.